Bitcoin Outlook: ETFs, Volatility, and $140K Path

February Drop and Market Resilience

Bitcoin shed 14.7% in February, testing $60K in the interim, and then was largely unfazed by the onset of the Middle East conflict earlier this month.

The token initially posted slight gains before correcting lower going into the end of March.

ETF Flows vs Safe-Haven Narrative

Notably, ETF inflows picked up as the Iran war broke out, totaling ~$450 mn on March 2 and ~$462 mn on March 4, and then normalized.

Bloomberg Intelligence said BTC could take over the safe-haven appeal from gold, as Bitcoin ETF inflows were paired by comparable outflows from gold funds.

Pushing back against this claim, we believe BTC is still far from being a so-called safe-haven asset.

$14B Options Expiry: Real Impact

The March 27 industry agenda will include the expiration of Bitcoin options totaling $14.16 bn.

Despite the massive volume, this event may not necessarily trigger sharp price swings, according to experts.

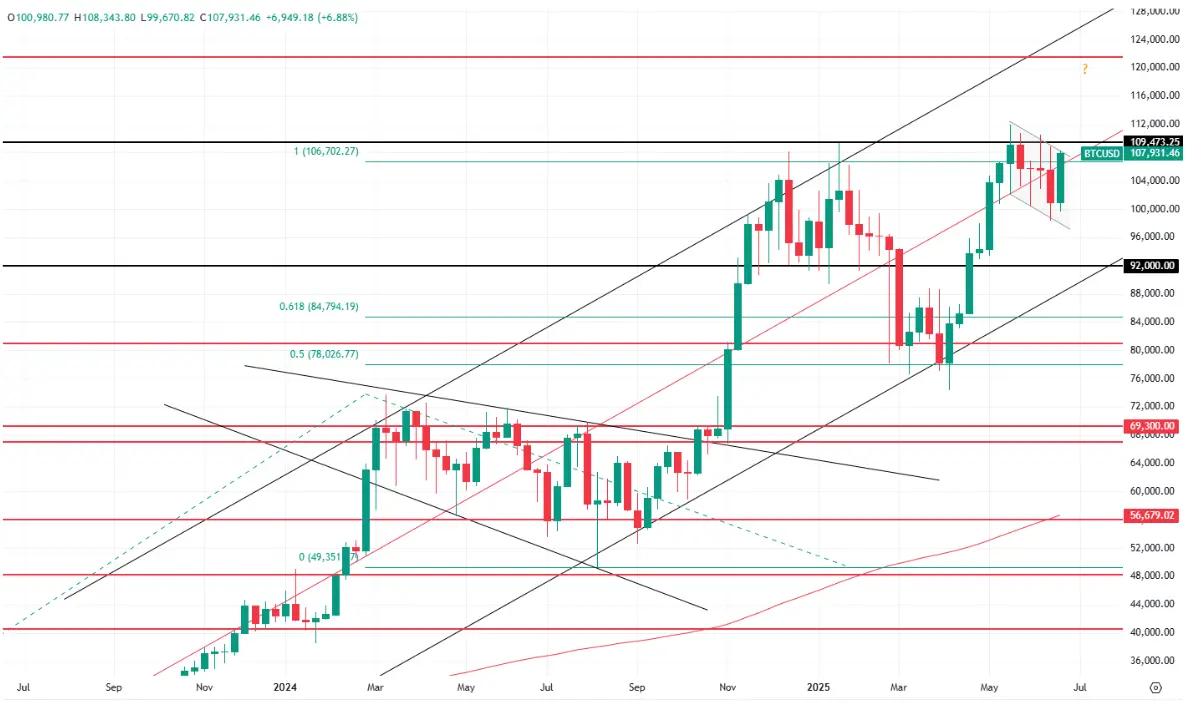

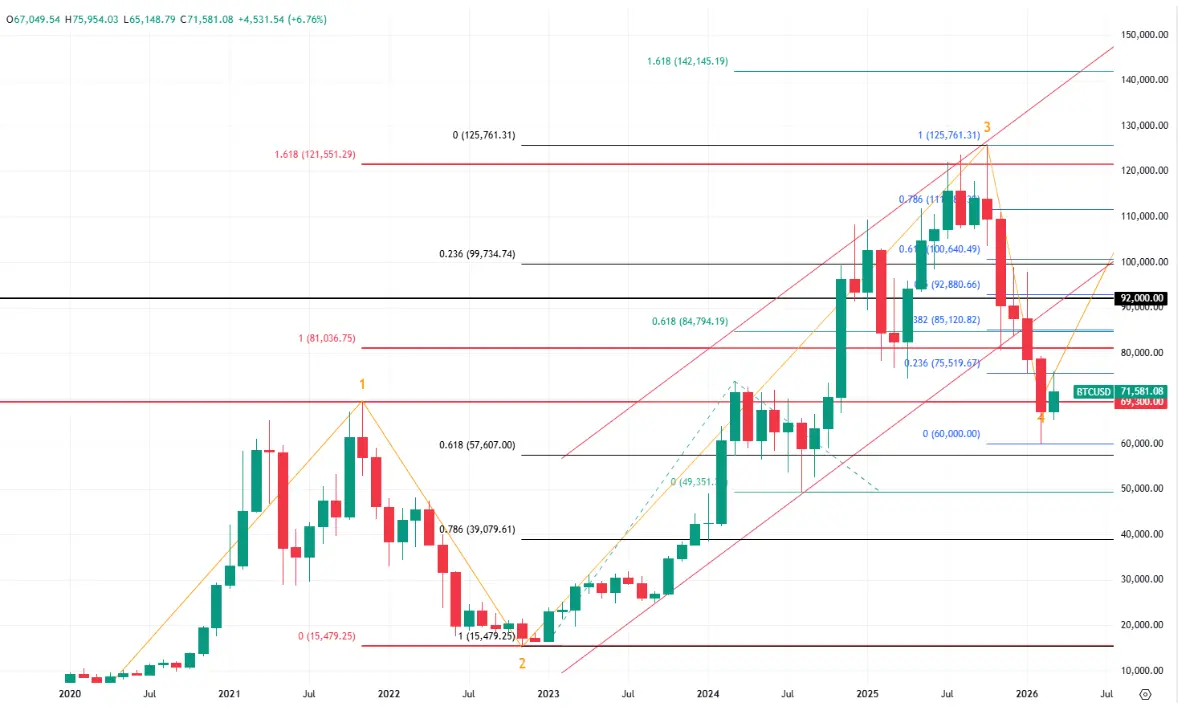

Elliott Wave Outlook: Wave 4 in Play

Technically, the longer-term monthly timeframe is better suited for classic Elliott Wave analysis.

To remind, our count includes the first impulse wave, which shaped up in 2020-2021 when the Bitcoin price climbed to a local high of $69.3K before lapsing into correction.

The second wave ended in November 2022 when the token dropped to $15.5K.

The third impulse wave was predictably the longest, reaching 161.8% of the first wave.

If our estimates are correct, this third wave ran topped out at above $125.7K.

Therefore, the price is now likely hovering within the fourth corrective wave, which could be nearing completion, as per the classical approach.

Under this scenario, the fifth and final impulse wave could be in the offing, set to match the length of either the first or the third wave, while not exceeding the latter.

We continue to adhere to a constructive outlook for Bitcoin, which still holds the potential to revisit the $120-127K range in the medium term and move towards $140K in the longer run.